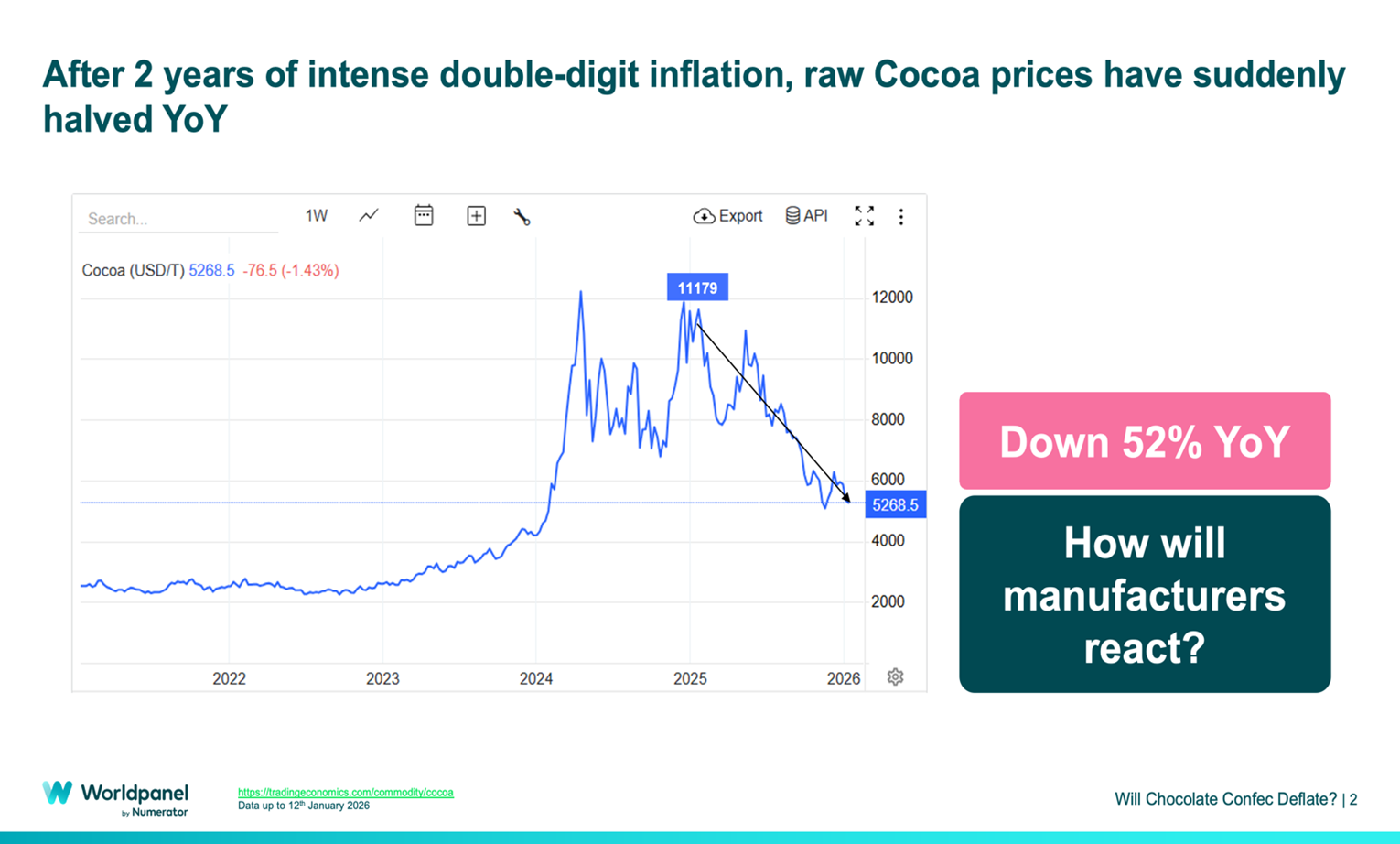

Cocoa is getting cheaper. That is the good news. The awkward news is that shoppers may not feel it, at least not in the way they expect.

After two years of punishing input inflation, cocoa prices have fallen sharply, roughly halving versus last year. Raw cocoa prices are down 52% year-on-year.

For chocolate manufacturers, that looks like relief: fewer sleepless nights about margin squeeze, fewer emergency price rises, fewer awkward conversations with retailers about “unavoidable” cost pressures. There have also been fewer conversations about protecting what has been a volatile supply chain. For shoppers, it sounds even simpler: cheaper cocoa should mean cheaper chocolate.

But a quick drop on the commodity chart rarely translates into a quick drop on the shelf. Over the past couple of years, the chocolate aisle has absorbed a series of increases that would once have been unthinkable. So, shoppers adjusted, and so did manufacturers. We saw shoppers buying smaller packs, often driven by manufacturers producing smaller options to help inflationary pressures on shoppers. We also saw switching of pack formats as buyers leaned harder on deals, and in some cases treated chocolate as a less frequent indulgence. Retailers adjusted too, building promotional calendars that helped keep the category moving while shelf prices climbed. The result is a new set of “normal” reference points that does not automatically unwind when input costs ease.

Deal Deluge

That is why the most plausible near-term outcome looks like this: promotions become the main theatre of competition. Everyday prices can stay sticky while deals become more frequent, more visible, and sometimes deeper. “Expect more deals, not cheaper chocolate” captures the feel of it. We saw similar dealmaking play out for coffee and other confectionary products. For Easter 2026, the same logic points to deeper deals and very familiar shelf prices.

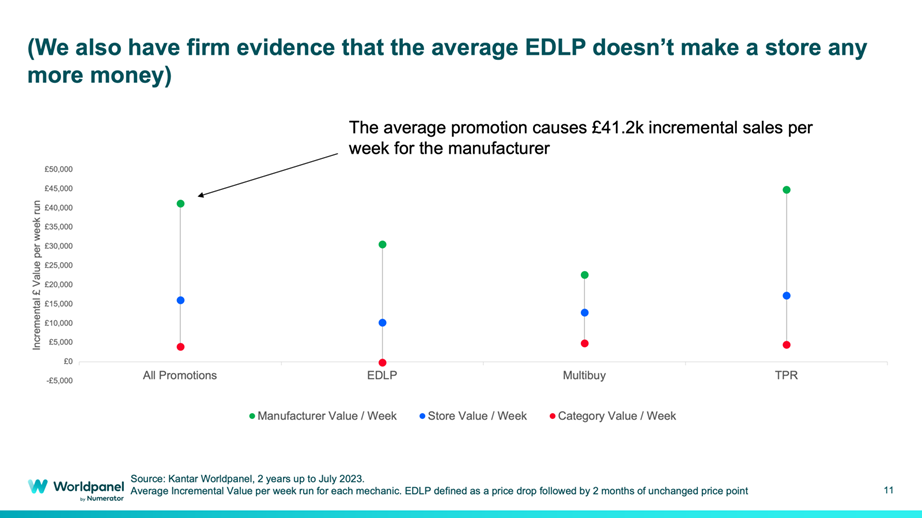

Helpfully for brands and retailers, promotions fit the reality of how chocolate is bought and sold, chocolate deals tend to create extra purchasing. A promotion week can increase basket add-ons and stock-up behaviour, and it can pull forward trips around seasonal moments. Across mechanics studied over two years, the average promotion delivered £41,200 of incremental sales per week for the manufacturer. In categories where margins have been tight , that kind of lever gets attention. As margins further improve with lower cocoa prices, this will be seen by many as encouraging news.

Promotions also align with how decisions get made inside businesses. Multibuys can be deployed where shoppers are primed to stock up, while straight price cuts can remove friction for entry-level buyers. That ability to tailor and adjust is valuable in an environment where costs, competition, and shopper confidence all remain fluid.

Cut-price Culture

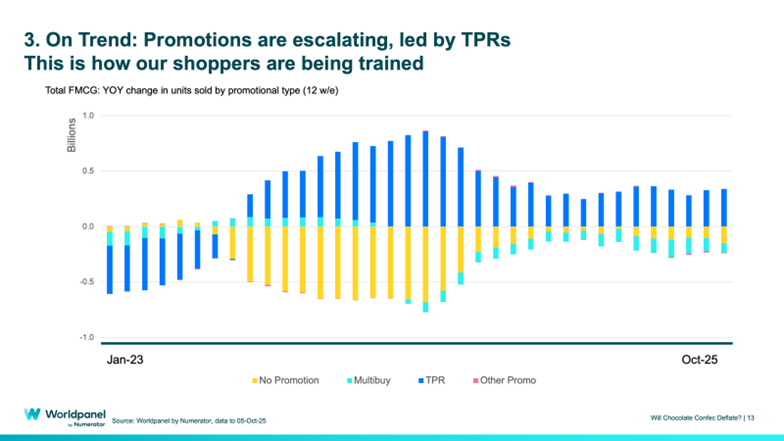

Another force is at work and must be handled with care. The market has been “training” shoppers to expect more promotional activity, led by straight price cuts. Across total FMCG, we have seen a large year-on-year swing towards temporary price reductions (TPRs), while non-promoted units fell significantly. TPRs have also grown in the wake of legislative multibuy restrictions for HFSS (high fat, sugar, salt) products. However brands fund it, and retailers plan for it, shoppers learn to wait for it.

Yet, none of this makes shelf deflation impossible. It tends to arrive when pressure builds in ways that are hard to ignore. We look for three signals indicating whether the market is drifting toward a point where the structure struggles to hold.

The first signal is volume. Value sales can look stable while households buy less product ., particularly so when propped up by inflation. Volume tells the more direct story: how much chocolate is leaving shelves. When volume weakens meaningfully, it suggests resistance that promotions are not fully offsetting. That scenario forces a broader response across pricing, pack architecture, and promotional strategy.

The second signal sits in private label price gaps . Supermarket own-label chocolate offers a credible alternative for many households. When the price gap between branded and private label widens beyond what shoppers feel is justified, switching accelerates. That shift shows up through share changes, penetration changes, and erosion of brand loyalty. Brands feel that pressure quickly, particularly in everyday formats where substitutability is high.

Value Gap

The third signal shows up in competitor gaps. In many chocolate segments, a close branded rival can provide a nearly interchangeable, or substitutable option. When one brand looks consistently better value, and is easily substitutable, shoppers migrate. Coca-Cola versus Pepsi is the classic example of this. Migration from one to the other may be slow at first, then fast once the gap becomes obvious and repeatedly reinforced through promotions or market positioning . Put simply: pricing strategy reacts to share movements .

These three signals shape how the cocoa story will play out in practice. Cheaper cocoa creates room for changes to the basket. The category decides how to use that room based on what shoppers and competitors are doing.

Recent history from adjacent categories hints at what this can look like. Coffee flipped from high inflation to deflation over 14 months. In the promotional pattern that followed, we saw the following: discount depth hovered around 5% higher, with steeper deals emerging as inflation softened. The shopper experience became more deal-rich, and everyday prices moved more cautiously.

Sugar Rush

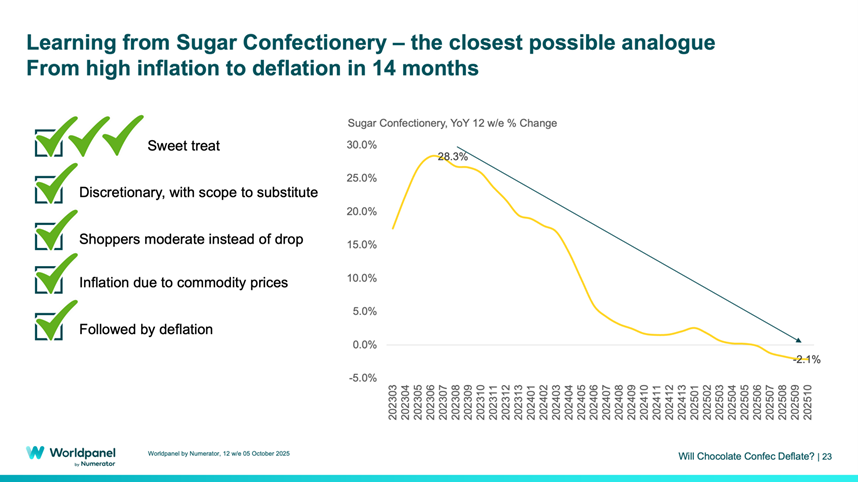

Sugar confectionery provides an even closer comparison. It followed a similar 14-month path from high inflation into deflation. Deal behaviour escalated rapidly as inflation eased. Worldpanel shows volume on deal moving from roughly 11% to 26%. We also witness a meaningful speed of manufacturer response: 54% more deals added in just three months.

The lesson for chocolate is straightforward: deal intensity can be a growth engine and can also reshape who buys the category and where.

Falling cocoa costs can support margin repair, fund stronger promotional mechanics, and enable targeted moves to close gaps where switching risk is rising. Promotions offer a practical way to do that because they can be aimed at the exact pressure points the market reveals, by retailer, by pack, and by moment.

That brings the conversation to strategy, because a promotion-heavy phase rewards discipline. Promotions can recruit, retain, defend, and grow, depending on how they are designed. Multibuys can build pantry loading; straight price cuts can reduce the barrier to entry; seasonal bundles can protect gifting occasions. But poor execution on promotions in these instances can train shoppers to wait and category value is undermined because the deals are subsidising what a shopper was going to buy anyway. With clarity, promotions support growth while preserving the shelf price architecture that the category has spent years building.

Samuel Hart

Business Unit Director, Worldpanel by Numerator

.svg)