Take-home sales at the grocers increased by 4.4% in the four weeks to 22 March 2026 compared with the same period last year according to our latest data.

As scrutiny over the impact of the conflict in the Middle East increases, the rate of like-for-like grocery inflation held steady at 4.3%. Even prior to the war, more than 20% of Britons described themselves as financially struggling* with over 60% very or extremely concerned about the rising price of groceries. Each additional 1% on the rate of inflation could add more than £50 to the annual supermarket bill for the average household. Additionally, 42% said they were worried about rising fuel prices – a proportion certain to increase as the cost of petrol and diesel have risen.

Financial anxiety among British consumers was already running high before the conflict began. And with grocery inflation likely to increase and fuel costs rising sharply, the conditions that make shoppers feel vulnerable are only intensifying. Shoppers will look to lessen the impact on their baskets when faced with rising prices, and while there remains a level of uncertainty, we are watching the data closely for behavioural changes like trading down and switching which often emerge during periods of economic pressure.

Easter eggs more expensive but shoppers not choosing smaller ones

With Easter fast approaching, just over 40% of shoppers have picked up at least one pack of hot cross buns in the past four weeks and 30% have bought at least one Easter egg, with a couple of weeks still to go in the run up to the bank holiday weekend.

While the pace of chocolate price inflation eased again – down to 8.0% from 9.3% last month – continued price pressures mean the average amount paid for an Easter egg was 9% higher than last year, up to £3.27. Despite this, there is no sign of shoppers choosing smaller eggs though, with an average weight of 162g, a marginal increase on last year.

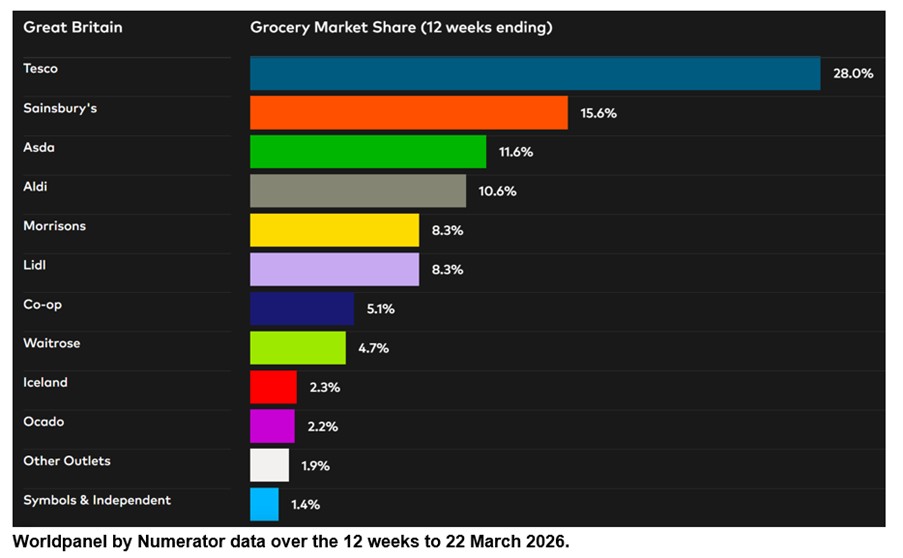

Lidl win the most market share while Ocado grow the fastest

Over the 12 weeks ending 22 March Lidl increased market share by 0.5 percentage points, more than any other grocer. Sales at the discounter rose 9.6% year on year, taking its share to 8.3% of the market. Online only retailer Ocado grew even faster, with sales rising by 12.3% and now accounting for 2.2% of the market, up from 2.0% in 2025.

Sainsburys attracted more new households than any other grocer, with 387,000 more customers through the door than in the same 12 weeks a year ago. At 5.5%, the retailer recorded its fastest growth since June 2025 with share moving from 15.3% last year to 15.6%. Tesco made the same share gain, an increase of 0.3 percentage points, giving them 28.0% of all sales. Spending through the tills of Britain’s largest supermarket was up by 5.0%.

Sales at both Aldi and Morrisons increased by 2.3%, resulting in a market share of 10.6% and 8.3% respectively. Asda hold 11.6% of the market with sales down 0.9%, but this does mark the best performance for the retailer since April 2024.

Higher average spending per trip drove 5.8% sales growth at Waitrose, the fastest rate of growth in five years, taking share up 0.1 percentage points to 4.7%. Co-op share stands at 5.1% and Iceland at 2.3%. Grocery sales at M&S**, which competes with the supermarkets, increased over the 12 weeks by 9.5%, the fastest since June last year.

*Worldpanel by Numerator Panel Voice Pressure Groups survey. 8,037 households interviewed in January 2026.

**Please note: with a higher proportion of clothing and general merchandise in its sales mix, M&S does not fall under the definition of ‘grocers’ using the Till Roll methodology on which the Worldpanel Grocery Market Share release is based. For this reason, a comparable market share number is not provided for M&S. The M&S growth number quoted in this update is for FMCG sales only, while the figures for grocers in the Grocery Market Share table cover total spending through supermarkets’ tills.

Fraser McKevitt

Head of Retail and Consumer Insight, Worldpanel by Numerator

.svg)