Commentary by

Business Unit Director

Worldpanel by Numerator

Brand loyalty has a lovely sound to it. A shopper walks down the aisle, passes every other pack, bottle, box and bag, and still reaches for yours. Every. Single. Time.

A marketer may call that devotion. A sales deck may call it proof of indispensability. A retailer may hear a subtle threat: take us off the shelf and these shoppers will walk.

The spreadsheet is less sentimental, and would probably call it exclusive buying behaviour.

That distinction is important to recognise. A shopper can buy one brand for all kinds of reasons. They may love it. Or, they may buy it on promotion. They may find it in the same store every week, in the same size, at a price that doesn’t require much thought. They may barely care about the category and buy the first acceptable thing their hand lands on. All of these things can be true. So we gave it a (much) closer look.

Worldpanel by Numerator’s analysis looks at shoppers who bought only one brand in a category over 52 weeks. We found that in some aisles, that behaviour is commercially valuable. In others, it is a habit dressed up as affection.

Spin cycle

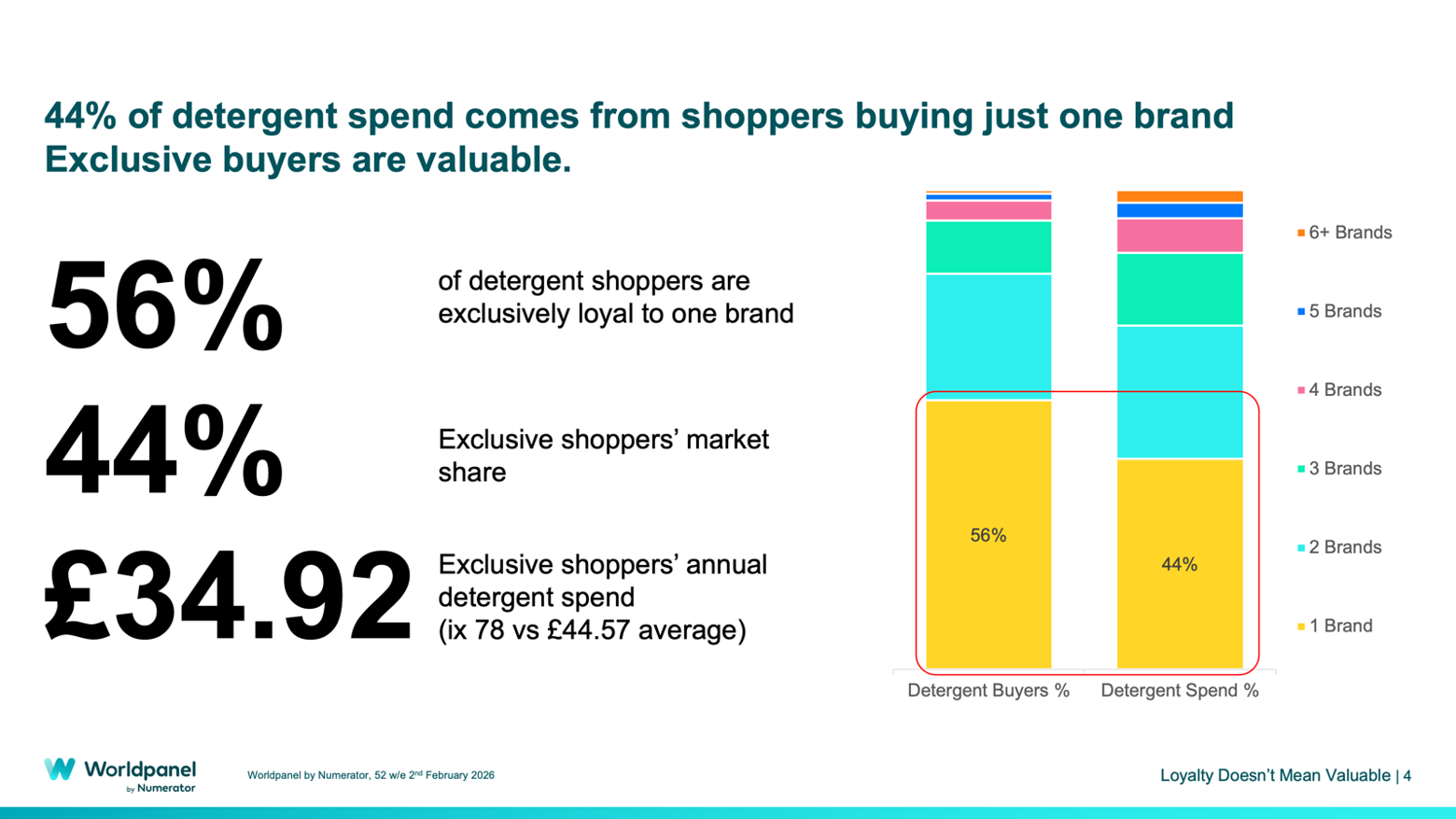

Laundry detergent is where the romance has some substance. In detergent, 56% of shoppers are exclusively buyers of one brand, and those shoppers account for 44% of category spend. Their average annual detergent spend is £34.92, indexing at 78 against the category average of £44.57. Persil has a real case here: exclusive buyers account for 21% of its value, worth £40m.

That makes sense. People don’t usually wander the laundry aisle for fun. They have a job to do. We want the basics: Clean clothes, a familiar scent, no strange residue, no surprises when the washing comes out. A detergent brand that becomes the default can be, like some stains, hard to shift because the category rewards certainty.

Choc and awe

Chocolate behaves like a different creature altogether.

Only 2.6% of chocolate shoppers are exclusively buyers of one brand. They account for just 0.2% of category spend. Their annual chocolate spend is £16.12, indexing at 9 against the category average of £177. The shopper who buys only one chocolate brand is often a very light category buyer. It may be that their loyalty may look pure simply because there isn’t much behaviour to examine.

That should make some brand plans sweat.

A chocolate brand chasing exclusive buyers may end up chasing people with little actual appetite for chocolate. Yes, you read that right. The richer prize likely sits elsewhere: the household with a crowded cupboard and several reasons to buy. A bar for the train. A pouch for the sofa. A multipack for the children. A seasonal pack because visitors are coming. Something new because the store fixture made it easy to say, “go on then.”

Aisle be back

The category structure explains much of the difference. Laundry detergent is concentrated. The top five detergent brands account for 75.6% of category spend. Chocolate is scattered across a much wider field, with the top five brands accounting for 26.4% of spend and all other brands accounting for 73.6%.

That’s just the chaotic reality of how the aisle works. Chocolate invites switching because the occasions keep changing. So do sweet biscuits, crisps, carbonated soft drinks and other categories built around mood, impulse, family need and small permission.

This leads to some inevitable truisms: exclusive loyal shoppers are least valuable in expandable and impulse-led categories: chocolate indexes at 11 versus the average shopper, sweet biscuits at 21, cereal at 24, crisps at 24 and carbonated soft drinks at 25. Planned household and personal care categories behave differently: shower products index at 59, laundry detergent at 69 and fabric conditioner at 78.

The commercial question changes by aisle. In a planned, functional category, exclusive buying can defend value. In a high-frequency, repertoire-led category, it can point to people who barely play in the category at all.

Frequency gives a useful warning. Chocolate shoppers buy the category 39.4 times a year. Sweet biscuits sit at 38.6. Crisps at 24.5. These are categories where life keeps changing the brief. Lunchboxes, evenings, guests, football, a bad day, a good one, a child with a favourite, a partner with a different one. A brand rarely wins by asking shoppers to abandon all others. It wins by getting into the set often enough to be chosen again.

Galaxy makes the point neatly. Repertoire buyers account for 88% of its value. The exclusive shopper is eight times harder to find. Across chocolate, shoppers buying 11 or more brands spend £250.57 a year on the category, compared with £16.11 among shoppers buying one brand.

Even heavy buying has a short shelf life. Half of Maltesers heavy shoppers are no longer heavy a year later. These shoppers are worth winning, of course. They just shouldn’t be treated like land that has been bought and fenced. In repertoire categories, brands have to earn the next occasion, then the one after that.

Shelf control

This should change how manufacturers talk to retailers. A claim about exclusive buyers needs a follow-up question: is that exclusivity valuable in this category, or is it light buying with a better suit on?

For detergent, exclusive buying can strengthen the listing argument. For chocolate, biscuits, crisps and soft drinks, the better commercial argument may sit with reach, occasions and repertoire. So, what does this look like? Get into more households. Give shoppers more reasons to pick the brand. Make it easier to choose when the mood, mission or household need changes.

I’d argue, our Brand Footprint rankings also should play a role. Consumer Reach Points show how often a brand is chosen across households. Exclusive buying shows whether a brand has a sole-buyer base. Those measures answer different questions. They should lead to different actions.

Pick your battles

Manufacturers should stop treating so-called loyalty as a virtue in itself. Loyalty has to pay its way like everything else on the shelf.

For many brands, the smarter fight is smaller: one more lunchbox, one more evening treat, one more shared bag, one more “go on then” at the fixture.

The loyal shopper may sound like the dream. In many categories, the shopper with a few favourites and a flexible hand is the one worth chasing.

.svg)