South Africa’s FMCG market reached R414 billion in the 12 months to December 2025, delivering +4.6% value growth and +3.3% volume growth year on year. Household consumption increased by +1.9%, supported by higher shopping frequency.

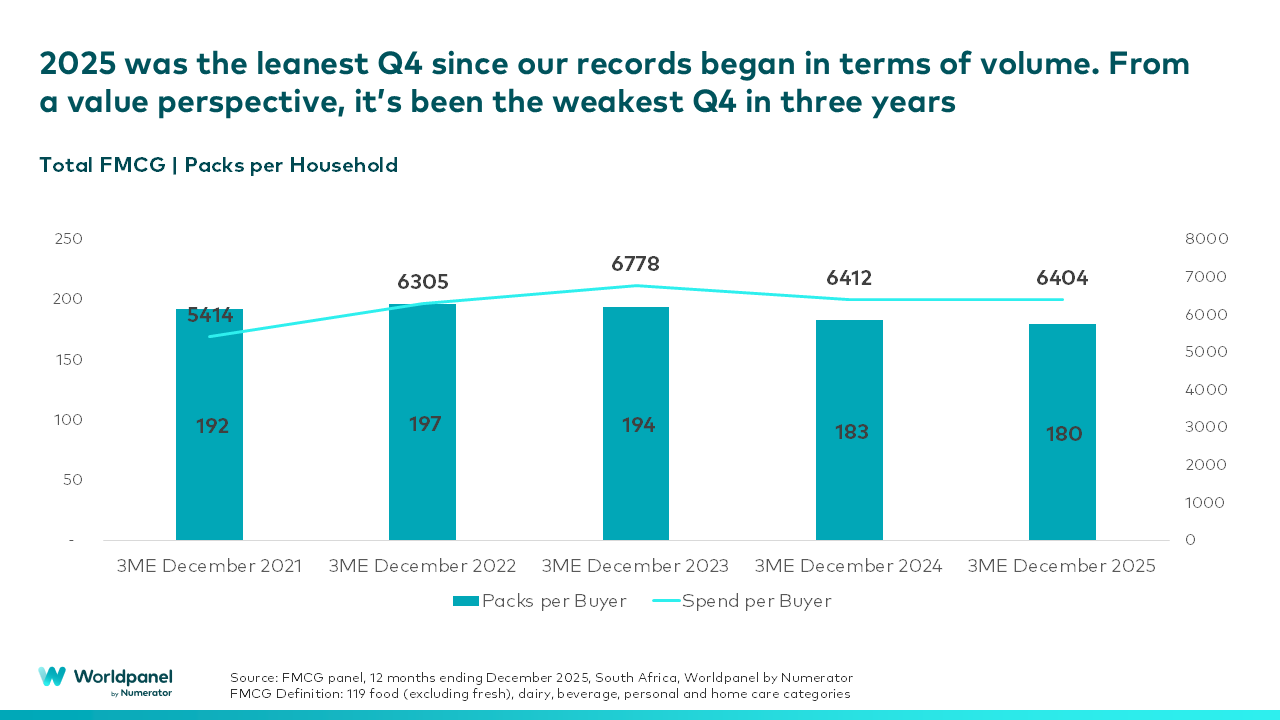

However, beneath the annual growth, a more cautious shopper story is emerging. Q4 2025 was the weakest fourth quarter on record in volume terms, with packs per buyer declining from 183 in Q4 2024 to 180, and packs per trip also falling from 6.69 to 6.50, confirming that shoppers are visiting stores more often, but purchasing fewer units per visit.

The result is a market growing in value, but with clear signs of tightening basket discipline.

Commenting on the findings, Vanessa Hall, Commercial Growth Partner at Worldpanel by Numerator South Africa, said: “South Africans are not buying less annually, which indicates they are buying smarter. Frequency is up, but every item now needs to earn its place in the basket. What we’re seeing is that consumers are becoming noticeably more careful and intentional with their FMCG spending.”

Volume pressure concentrated in specific sectors

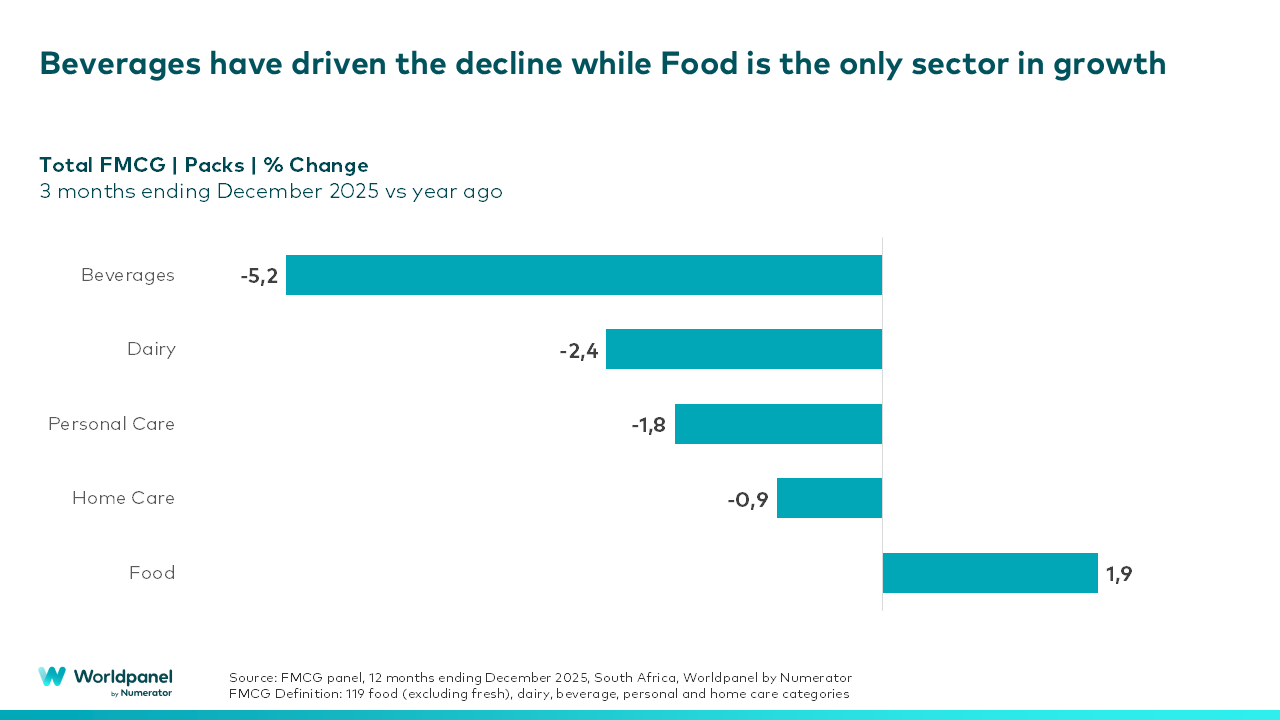

The slowdown is not evenly distributed. In the last quarter of 2025:

- Beverages declined -5.2% in volume, driven primarily by alcohol and juice concentrates

- Food delivered +1.9% volume growth, making it the only macro sector in positive territory

- Dairy, Home Care and Personal Care recorded softer volume trends, largely due to reductions in units per buyer

Over a longer-term view (December 2022–2025), beverages show the most sustained rationalisation, suggesting this is not a short-term fluctuation but an ongoing behavioural shift.

Importantly, households are not exiting categories wholesale. Instead, they are buying into slightly more categories year on year, while reducing volume within each. This indicates deliberate basket optimisation rather than retreat from consumption.

Large brands face mounting value pressure

At brand level, structural pressure is becoming clearer. In some cases, established leader brands are, on average, losing volume share, while lower-priced challenger brands are gaining traction across multiple categories. Notably, this is not primarily a Private Label story – Private Label value share has remained broadly stable over the past 18 months. This divergence suggests that in 2026, brand growth will likely depend on accessible pricing architecture and clearly differentiated value delivery, rather than scale alone.

Retail dynamics reflect mission-based spending

Retail performance mirrors the same behavioural tightening. Supermarkets continue to account for the majority of FMCG value, although share has softened over time. Independent retailers continue to outperform total market growth rates.

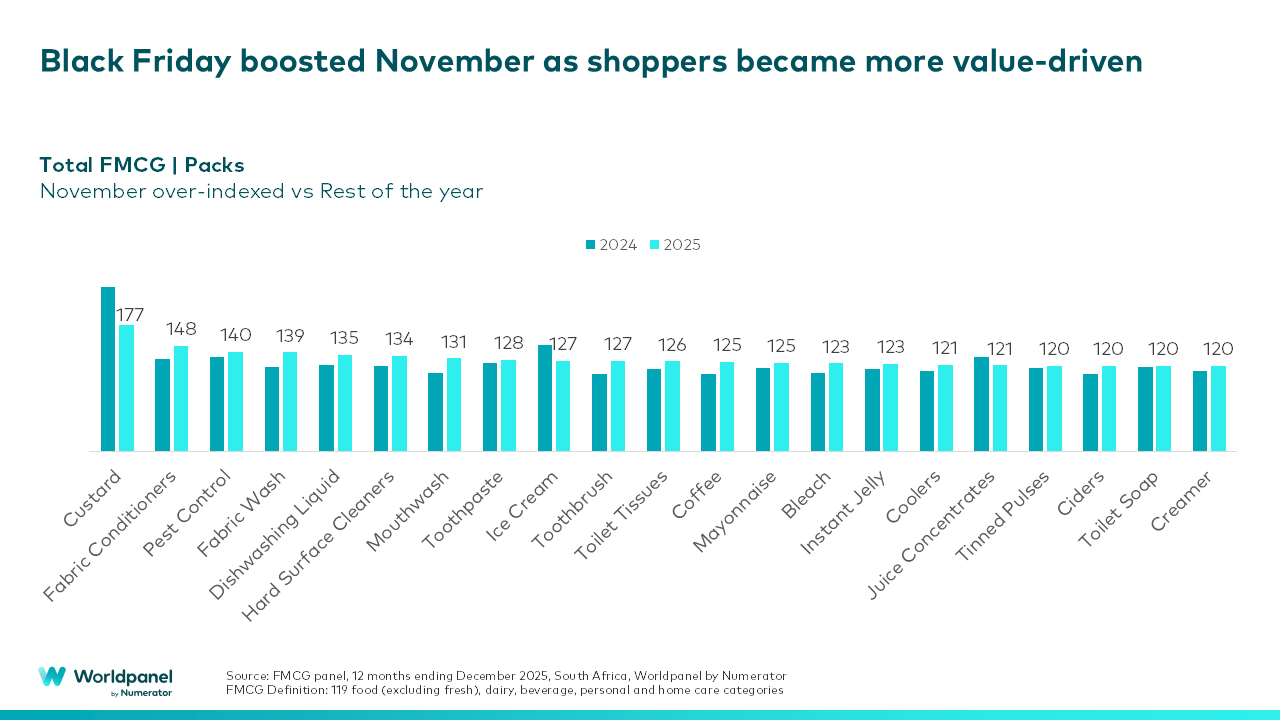

November spend over-indexed versus the rest of the year, supported by Black Friday, while both October and December underperformed in volume terms. These patterns indicate that shopper engagement remains high – but spend is increasingly value-driven, tactical and mission-specific.

Hall concludes: “For brands and retailers, the opportunity in 2026 will not be about chasing volume at any cost. The consistent theme is rationalisation, not retreat. Success in 2026 will depend on delivering clear, accessible value and understanding the missions that now shape household spend.”

If you’d like the full State of the Nation report or expert guidance on how these trends should shape your brand’s 2026 strategy, get in touch – our team is ready to help.

Vanessa Hall

Commercial Growth Partner South Africa, Worldpanel by Numerator

.svg)