Did you miss the first article in this series? We invite you to explore the three consumer segments driving these changes, and what they reveal about the future of value in the UAE, before continuing with this second part.

While UAE households differ sharply in outlook, their behaviours are converging around one theme: greater intentionality in everyday spending. A new nationwide survey by Worldpanel by Numerator shows how shifting mindsets are already influencing routines, seasonal behaviour and category performance across FMCG.

Understanding these behavioural expressions is critical for brands navigating an environment where volume pressure, promotion sensitivity and selective spending coexist.

Everyday routines are tightening

Across segments, households report scaling back discretionary activities. Dining out, social occasions and food delivery are all declining as families focus spending closer to home.

More than two-thirds of households say they have changed daily routines in response to current conditions. For some, this is driven by necessity, for others, by a desire for control and predictability. Either way, everyday consumption is becoming more home-centred and more intentional.

“Price sensitivity is rising across the board, but especially among The Burdened segment, where willingness to switch brands or delay purchases is highest,” says Karan Gupta, Solutions Director, Advanced Analytics, Worldpanel by Numerator Africa & Middle East. “This creates immediate pressure on loyalty-based growth models.”

Ramadan becomes more family-centric than social

Seasonal behaviour reflects this shift clearly. During Ramadan, social activities such as visiting friends, attending events and going out for iftars declined compared with previous years.

At the same time, the Routine Protectors and Calm Calculators segments increased grocery stock-ups, reinforcing the role of the home as the centre of family life. Even when overall spend is controlled, pantry loading remains a priority, particularly for categories linked to daily meals and routine moments.

This pattern highlights a move away from outward celebration towards inward stability – a key signal of how emotional priorities are evolving.

Categories under pressure – and those that remain protected

Our nationwide survey of 1,294 main household shoppers shows that pressure is not evenly distributed across FMCG. Discretionary and treat-led categories face the highest risk across segments, including:

Beverages such as carbonated soft drinks, RTD juices, iced tea and energy drinks

Snacks, confectionery and chocolates

Selected frozen and convenience foods

These categories are most exposed to cutbacks, brand switching or reduced purchase frequency.

In contrast, essential and routine-anchoring products – such as staples, core dairy, cooking basics, and everyday home and personal care – remain relatively protected. These continue to play a stabilising role in household spending, particularly for families focused on maintaining normality.

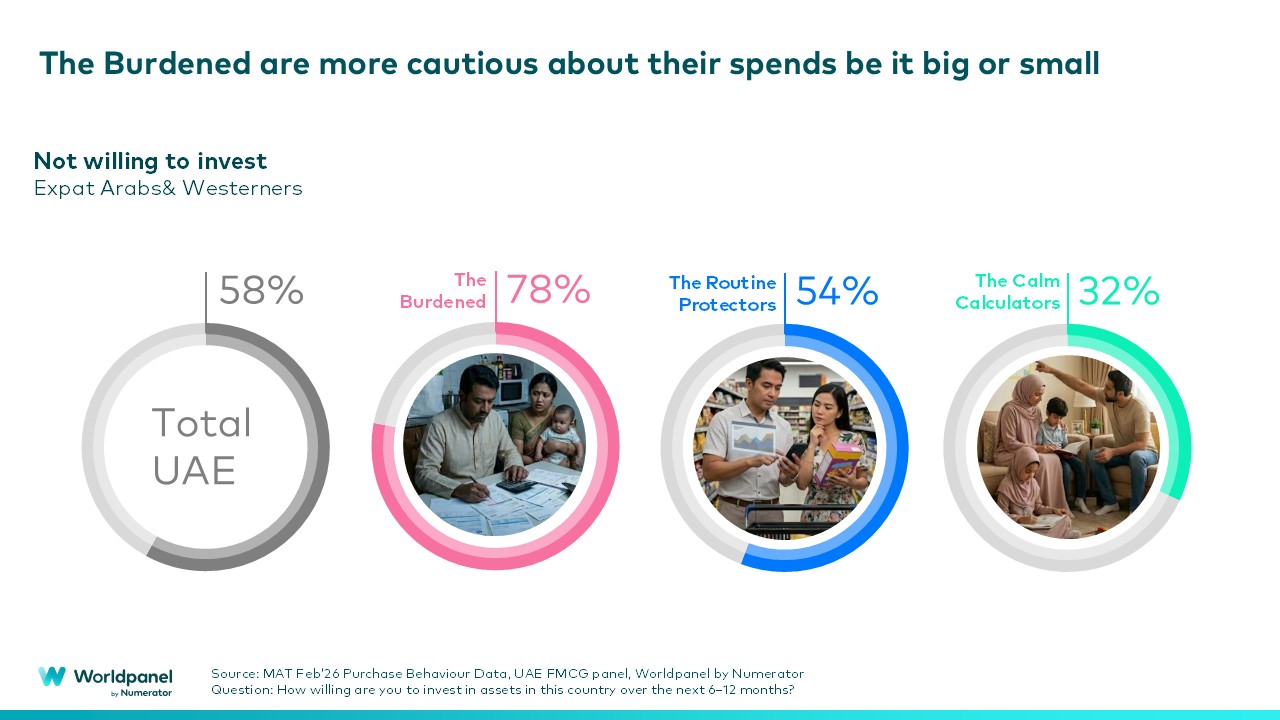

Caution extends beyond the shopping basket

Beyond FMCG, the research points to a broader shift in financial mindset. Many households, especially The Burdened, are delaying or avoiding longer-term commitments and investments.

However, despite this caution, most households still report feeling safe and stable living in the UAE. Rather than panic, the prevailing mood is one of measured restraint – adjusting spend today while keeping future options open.

What this means for brands

Together with the segmentation outlined in the first article, these behavioural shifts reinforce a clear message: growth strategies must be more targeted, emotionally aware and context-specific.

Winning in the current UAE market means understanding not just what consumers are buying less of, but why – and how those motivations differ by household mindset.

If you would like to learn more about the findings of this survey and what they mean for your brand and category, get in touch with our local experts.

Karan Gupta

Solutions Director, Advanced Analytics

Worldpanel by Numerator Africa & Middle East

.svg)