At a macroeconomic level, Vietnam’s position is relativelystrong. 2025 closed with GDP growth hitting the government’s target, supportedby a steady rise in average monthly income per capita of roughly +7% CAGR since2020, and a policy stance that was geared towards stimulating domesticconsumption.

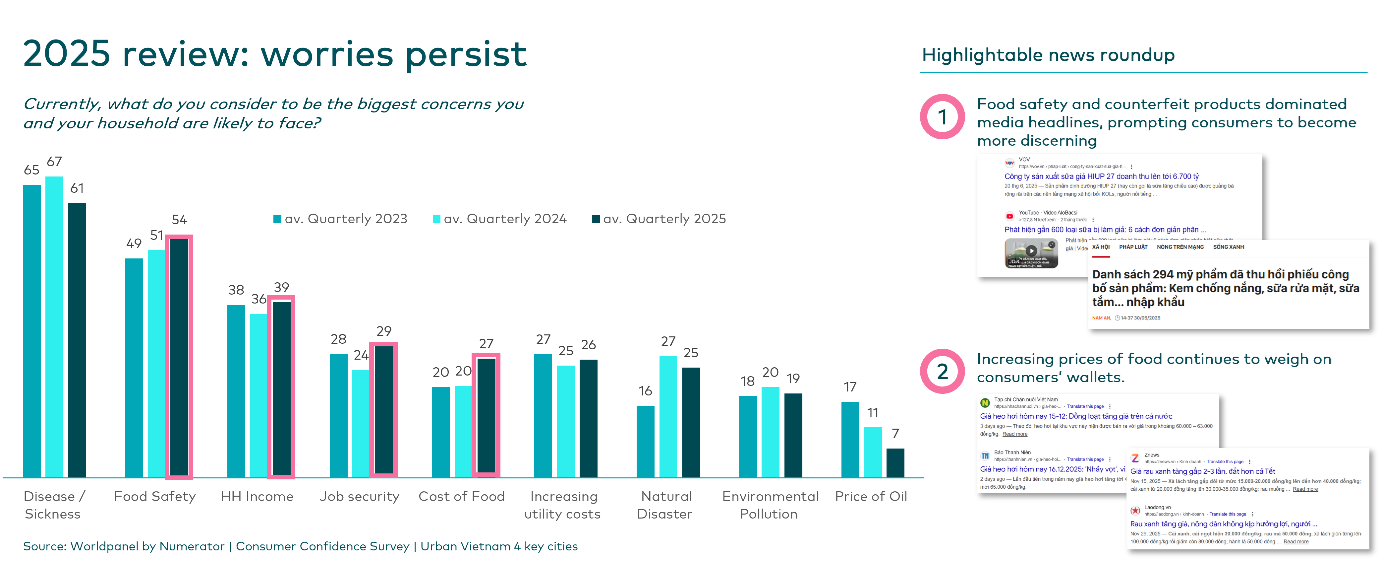

Yet this macro resilience does not automatically translateinto consumer confidence at the checkout. Recent months have seen Vietnameseshoppers become markedly more cautious, with food safety and counterfeitproducts dominating headlines and reshaping purchase criteria toward ‘trustsignals’ and stricter brand scrutiny. At the same time, the rising cost of foodcontinues to weigh on household budgets, compounding persistent anxieties aboutday‑to‑day living expenses.

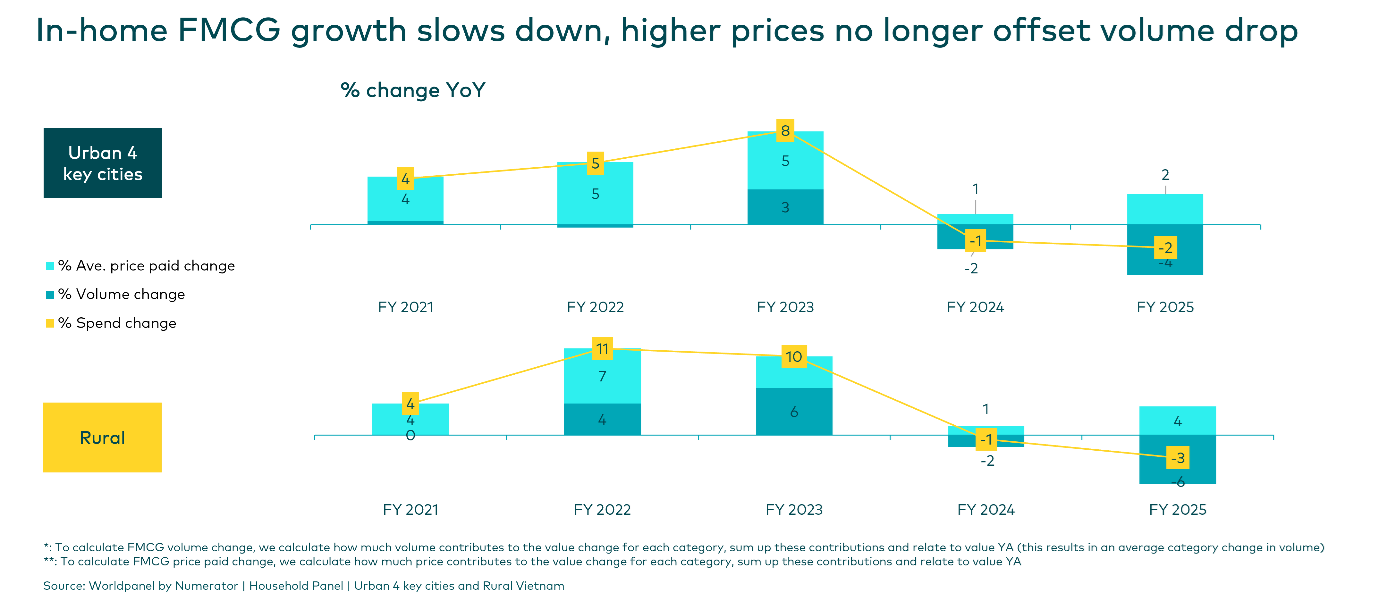

Volume is falling – and price can no longermask it

Forthe first time in several years, in‑homeFMCG value growth has turned negative. Brandsare facing a tougher reality: price increases alone won’t restore growth.

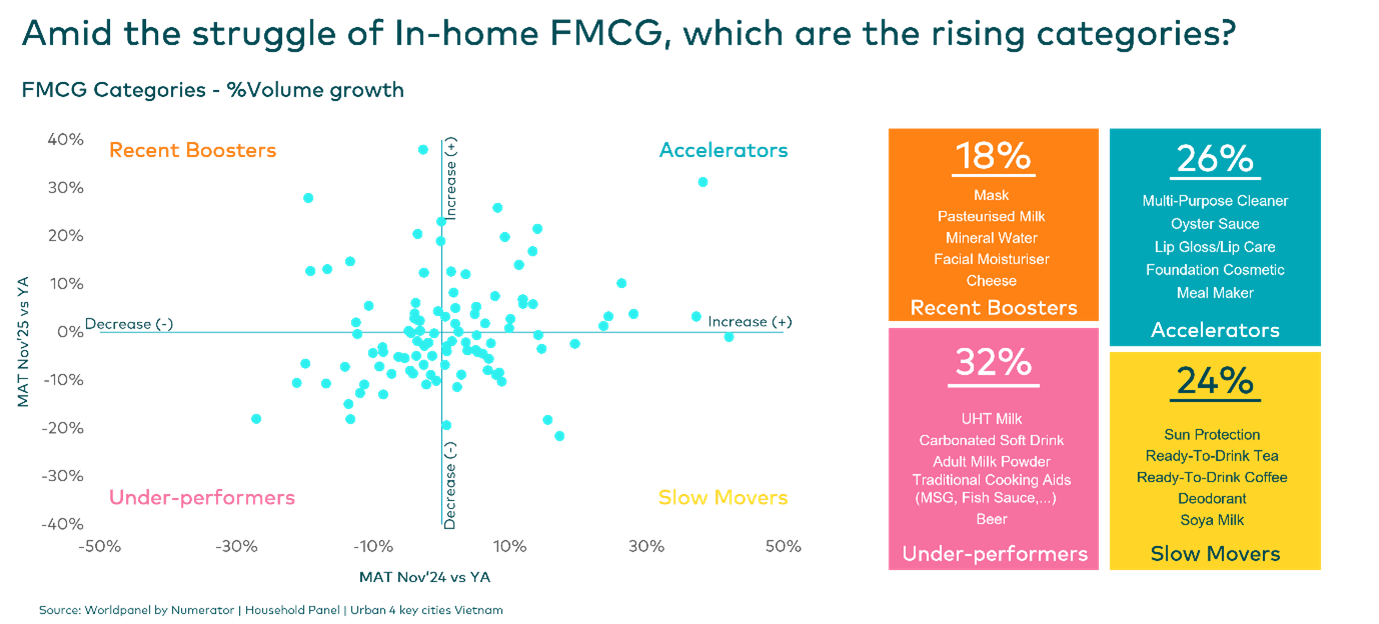

Bothurban and rural areas have seen volume declines, led by Dairy, Beverages, andPackaged Foods, where fewer celebratory occasions and an intensified scrutiny ofquality are reshaping demand. Yet the slowdown is not uniform.

Ourcategory mapping shows clear pockets of resilience: ‘Accelerator’ categories which make up 26% of the market – and ‘RecentBoosters’ (18%) tend to win by solving health, beauty or convenience-led needs.Meanwhile ‘Under‑performers’(32%) are more exposed to headwinds linked to value pressure and negativepublicity around quality, or counterfeit products.

With competitive disruption rising, the question for theremainder of 2026 becomes: how do you sharpen WHO to target, WHYyou are chosen, WHAT to prioritise, and WHERE to win? The answerlies in the Four Pillars for Brand Growth.

.svg)