Take-home sales growth at the grocers increased by 1.5% in the four weeks to 17 May 2026, according to the latest data from Worldpanel by Numerator. Inflationary pressures at the supermarket tills eased for shoppers, with like-for-like grocery prices rising by 3.1%, the slowest rate of increase since December 2024. The easing in the rate of inflation is welcome news for shoppers who have been grappling with warnings of a hike in food prices due to the impact of the war in the Middle East.

This follows the UK government's announcement on a plan to further reduce import tariffs by £150 million on a range of food categories. While further details are expected this week, this would equate to just £5 per household, with the average annual shopping bill for food and drink, excluding alcohol, totalling £4,087.

Shoppers leant on promotions to keep costs down, with 30.3% of sales including a deal last month – up from 28.4% a year ago. Spending on promoted items rose 9.5% year on year, while full price spending was virtually flat, growing by only 0.1%.

Shoppers opt for soup over suncream

Grey skies over the early May Day bank holiday weekend were a far cry from the current heatwave, and categories felt them impact over the month. While volumes of summer essentials like suncare and ice cream were down 28% and 3% respectively, warming staples found their way into baskets with soups up 9%, fresh pies up 4% and coffee up 5% year on year.

May was a tale of two bank holidays. The cool start kept summer categories in the shade, with unseasonable weather hanging on longer than expected. But with record temperatures over the second bank holiday, we expect to see a significant uplift in spending on summer essentials like BBQ, suncare and ice cream as the month comes to a close.

Ocado and Lidl the fastest growing grocers

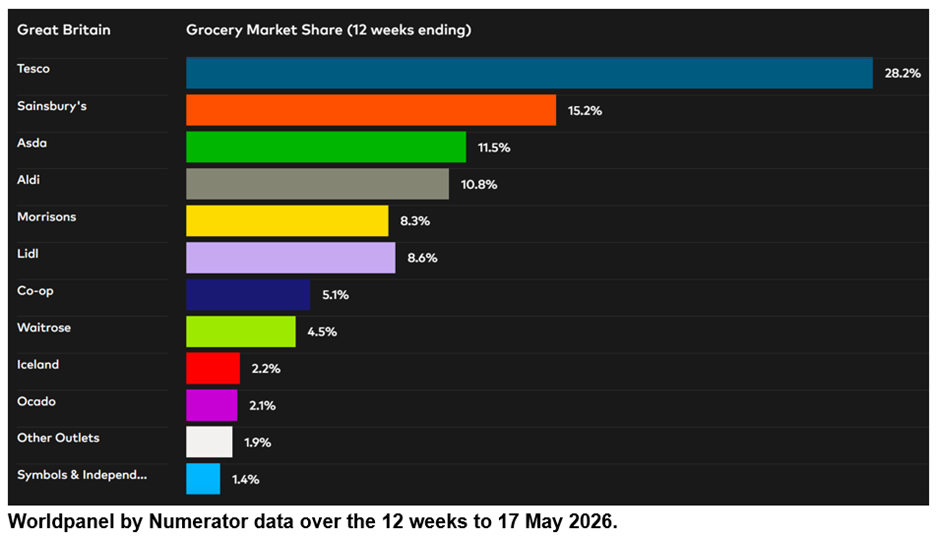

Lidl reached a new record high market share of 8.6% over the 12 weeks to 17 May, up by 0.5 percentage points compared to the same period last year. As a result, for the first time, Lidl secured its position as Britain’s fifth largest grocer. Twenty-five years ago, the retailer accounted for just 1.4% of the market, behind long gone names such as Safeway, Somerfield and Kwiksave.

Sales at Tesco increased by 3.2%, with market share rising to 28.2%, up from 27.9% in 2025. Sainsbury’s share was 0.1 percentage point higher than last year at 15.2% with sales growing by 3.1%. The market share of Asda now stands at 11.5%, ahead of Aldi at 10.8% and Morrisons at 8.3%.

Waitrose sales were up 3.0% while market share held steady 4.5%. M&S* grocery sales increased over the 12 weeks by 9.3%. Co-op market share now stands at 5.1% and Iceland 2.2%.

Ocado continued to be the fastest growing grocer with sales up by 10.2%, though this is the slowest recorded rate of growth for the specialist since July 2024. Market share for the online only specialist was 0.1 percentage point higher at 2.1%. Overall online sales for all retailers rose by 7.2% over the same 12 weeks.

*Please note: with a higher proportion of clothing and general merchandise in its sales mix, M&S does not fall under the definition of ‘grocers’ using the Till Roll methodology on which the Worldpanel Grocery Market Share release is based. For this reason, a comparable market share number is not provided for M&S. The M&S growth number quoted in this update is for FMCG sales only, while the figures for grocers in the Grocery Market Share table cover total spending through supermarkets’ tills.

Fraser McKevitt

Head of Retail and Consumer Insight, Worldpanel by Numerator

.svg)